by News Reporter April 10th, 2026

Canadian Farmland Values 2025 Show Distinct Regional Trends

Canadian farmland continues to demonstrate its position as a stable, long-term investment, supported by strong fundamentals such as limited supply, global food demand, and resilient farm balance sheets. However, recent data from Farm Credit Canada (FCC) highlights an increasingly regionalized performance landscape, with notable contrasts between the Prairies and provinces such as Ontario and New Brunswick.

A Strong National Trend—But Slowing Momentum

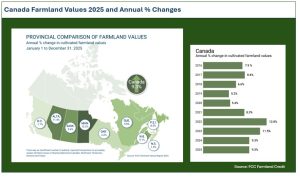

Over the past decade, farmland values in Canada have more than doubled, reflecting sustained demand for productive agricultural land. In 2025, cultivated farmland values increased by 9.3% nationally, continuing a growth streak of more than 30 years.

This continued appreciation underscores farmland’s attractiveness as a tangible asset with inflation-hedging characteristics, even in the context of softer commodity prices.

Prairie Provinces Lead Growth

The strongest gains in farmland values are currently concentrated in Western Canada. According to FCC:

– Manitoba: +12.2%

– Alberta: +11.4%

– Saskatchewan: +9.4%

These provinces drove national growth due to a combination of:

– Lower entry prices compared to Eastern Canada

– Large-scale, expansion-oriented farming operations

– Strong competition for contiguous land parcels

– High producer reinvestment capacity despite interest rate pressures.

FCC emphasizes that demand remained strong even in a higher interest rate environment, supported by long-term confidence in agriculture and constrained land supply.

In short, the Prairies continue to offer growth-driven investment opportunities, particularly for scale-oriented farming models. However, restrictions on foreign ownership in these provinces significantly limit access for foreign farmland investors.

Ontario: High Values, but a Pause in Growth

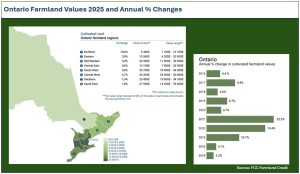

In contrast, Ontario experienced a notable slowdown in 2025, with FCC reporting near-flat or very modest growth.

Key drivers of this stabilization include:

– A period of strong price appreciation in previous years

– Reduced affordability at historically high land values

– Softer commodity margins in some crop sectors

– Increased sensitivity to interest rates.

Importantly, FCC frames this not as a decline, but as a market normalization phase after years of strong expansion.

Despite flat short-term growth, demand remains structurally strong due to limited land availability and long-term confidence in agriculture.

Unlike the Canadian Prairies, Ontario has no restrictions on foreign ownership of farmland, making it one of the most attractive jurisdictions in Canada for international investors.

Southwestern Ontario: Canada’s Premium Farmland Market

Within Ontario, Southwestern Ontario remains the country’s most valuable and strategically important agricultural corridor.

Key characteristics include:

– Class 1 and 2 soils among the most productive in Canada

– Intensive corn, soybean, and specialty crop production

– Strong proximity to U.S. markets and processing infrastructure

– Persistent land scarcity and development pressure.

Even in a flat growth environment, FCC data confirms that this region remains structurally supported by scarcity and productivity, making it a core institutional-grade farmland market.

New Brunswick: Emerging Value and Niche Strength

New Brunswick is highlighted in the FCC 2025 report as one of the stronger performers in Eastern Canada, with gains of over 9%.

This performance reflects:

– Tight land supply in productive agricultural zones

– Strong specialty crop sectors (notably potatoes and blueberries)

– Established agri-food ecosystem anchored by processors such as McCain Foods

– Increasing interprovincial and international farmer participation.

While smaller and less liquid than Ontario or the Prairies, New Brunswick is emerging as a value-oriented entry market with long-term upside potential. Importantly, the provinve also permits foreign ownership of farmland, enhancing its accessibility for international investors.

Outlook: Stability with Regional Divergence

Looking ahead, the Canadian farmland market is expected to remain stable but increasingly differentiated by region:

– Prairies: Continued growth potential, supported by affordability and scale, but limited accessibility for foreign investors.

– Ontario: Stable, high-value market with moderate growth.

Southwestern Ontario: Core premium region with strong long-term fundamentals.

– New Brunswick: Emerging value driven by specialty crops and lower entry pricing.

While short-term conditions – such as commodity cycles or interest rates – may influence transaction activity, the long-term outlook remains positive.

For international investors, Ontario and New Brunswick stand out as accessible and strategically complementary markets, offering both stability and growth potential.

Conclusion

Canadian farmland continues to offer a compelling investment profile, combining capital preservation, steady appreciation, and exposure to global food demand.

Ontario, and particularly Southwestern Ontario, represents a mature, high-value core market, where scarcity and productivity underpin long-term value. At the same time, New Brunswick provides emerging opportunities for investors seeking accessible entry points and diversification within Canada’s agricultural landscape.

For foreign investors, the key takeaway is clear:

– Performance in Canadian farmland is no longer uniform—understanding regional dynamics is essential to capturing value.

– Local support, as provided by FIAN, is essential for identifying opportunities and ensuring compliance with local regulations.

2026 © FIAN Inc.

For additional information about Canadian Farmland, please refer to FIAN’s Resource page.